When COVID-19 hit, it hit hard. Who would have imagined the Federal Reserves slashing interest rates down to zero to salve a dead stopped economy? Or imagined a worldwide lockdown? The modern world has, literally, never seen anything like this.

Like every other industry, VC funds have been forced to respond to the current meltdown. Many startup portfolios are in distress. According to recent surveys, 41% of global startups have less than three months of cash and 65% have less than six months cash in hand.

As one of the most active early-stage VCs, we wanted to better understand how our portfolio companies have responded to the crisis. To that end, our funds Joyance Partners and Social Starts have collected data through portfolio interviews, office hours, and surveys. The results proved fascinating and useful in evaluating portfolio management as a whole.

The Data

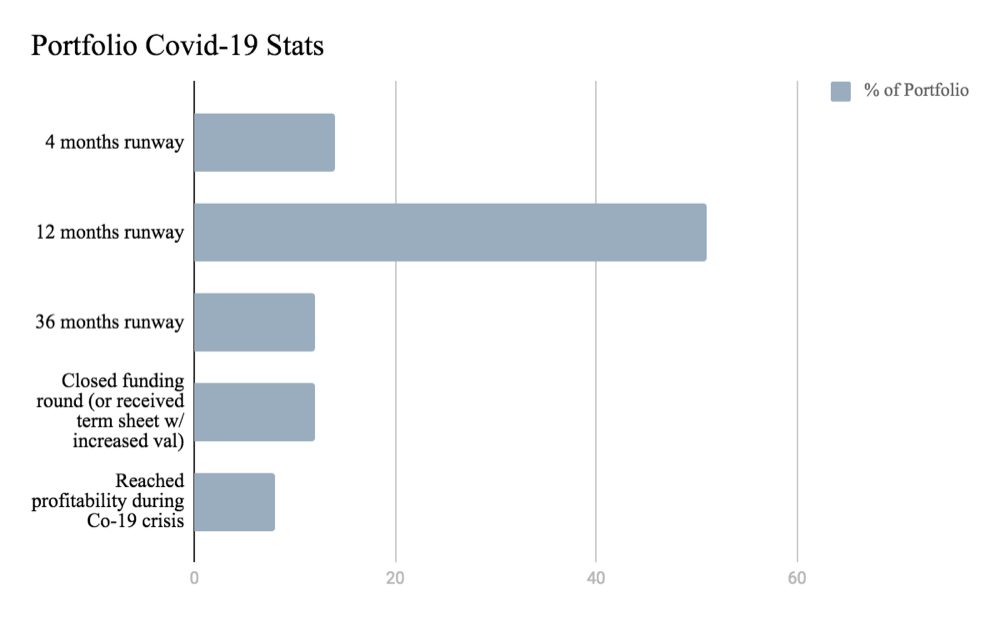

Among 203 active portfolio companies, we’ve collected over 90% of company data. The results:

-

14% of companies in the portfolio have less than 4 months of runway

-

54% have over 12 months of runway

-

12% have over 36 months of runway

-

12% have closed a new funding round or have received a term sheet with an increased valuation in the past three months

-

8% reached profitability during COVID-19 crisis

It’s extremely gratifying to see nearly half of our active portfolio companies are safe for at least the next 12 months. And we are delighted so many companies have even thrived during this crisis.

Why are we doing better than many funds?

First, let’s take a look at the big picture:

Who’s down?

-

Those whose supply chain and customers have been hammered by the crisis.

-

Those who had poor financial management before the crisis or believed in the inevitability of their next round.

Who’s up?

-

Those already on the digitalization path in health and happiness (AI-driven personal care, telemedicine, digital mental health and comfort platforms).

-

Those whose CEOs focused on strong fundamentals and long-term value creation, even before the crisis.

-

Consumer goods companies delivering ways to make homes more pleasant and useful, goods that offer greater control of food and other fundamentals, or small emotional wins.

Happily, and not by happenstance, we have a lot of “ups” in our portfolio. We feel we are seeing a clear benefit of our unique investment approach.

Semi-annually, our investment team tears down our funds and rebuilds them based on deep research across industries worldwide. We are seeking signals of the sectors with the strongest potential for high-value Series A rounds. A few years ago, all the data and signals pointed towards investing in health, personal happiness, education, and sustainability. We believed these sectors would become prime drivers of our global economy. The rising generation, we felt, would adopt innovations in these areas, driving strong growth that would persist over the next decades, even during economic turmoil. In other words, our methodology seeks endurability in our key sectors, and we think the current crisis shows we found it.

Health

When Joyance Partners was created, we saw the coming transformation of healthcare, spurred by one of the broadest set of scientific breakthroughs we had ever seen (e.g. CRISPR, sensor miniaturization, massive datasets driving deeper AIs, VR, and other new brain tools), and accelerated by a deep shift from consumers wanting to control their own health so they could pursue happiness as they defined it. Therefore, we set digital health as one of the core areas of investment. We had faith we would win, but expected it would be a long haul.

The current crisis, though devastating, has accelerated the adoption of digital health and lowered the barrier to entry and regulatory risks. It has pulled the future we anticipated forward, to the benefit of many of our companies. This is true of almost all our digital health sub-domains, such as AI chronic disease management (Lark, Digbi Health), remote monitoring (Gyant), digital therapeutics (GrayMatters), digital senior care, (Nymbl Health), telehealth (Dr. Sam) and personalized care (Thryve). The strongest companies in this area have significant IP and were already making progress, but have leaned aggressively into the COVID-19 opportunities presented by stressed hospitals to expand and grow in new ways. Lark, for example, has done an incredible job creating AI-only nurses that can handle care for chronic conditions like diabetes so perfectly that it qualifies for current human RN insurance codes. Now, Lark is poised for further dramatic growth because their beleaguered hospital customers are asking them to take over all diabetes and other disease care. The hospitals don’t have the current capacity for the work and don’t want chronic patients in COVID-active hospitals.

Personal Happiness

Restaurants are closed and people are worried about their immune systems. That means delivery services have surged, and people have started caring about their nutrition in a way we had only seen glimpses of in higher-income segments. Homegrown greens companies like Hamama have surged, alongside companies like Copper Cow Coffee. Even home design and decorating have surged for those prepared with inventory and a finger on the pulse of stir-crazy consumers at home like Outer. We were particularly pleased to see companies in tough categories like cosmetics and cookware rise to the challenge by creating hand tonic (Loli) and COVID-branded products (Made-In), in an attempt to stay top of mind. The big consumer goods winner we have seen during COVID, though, has been sexual wellness. The entire category has (additional source: Vogue) as people became isolated and anxious. Unbound is a pioneer in this space, helping transform what was once considered crude and distasteful into a reputable investment category and an outstanding investment vertical. This category is all about manufacturing diversification and supply chain control. Companies like Unbound have been able to thrive during COVID by juggling 10+ manufacturers globally for well-managed stock. As demand spiked, the companies who have been able to maintain “business-as-usual” have harvested the increased demand. The companies that struggled here didn’t have enough stock to respond to orders, were too focused on brick-and-mortar, or had to cut burn significantly to as an offshoot of cash crunches in part due to the longer raise cycles imposed by some later stage VCs and their need to seek big raise and valuation increases (additional source: Business Insider).

Education

Needless to say, parents and students out there have struggled during COVID to figure out how to continue their education. However, change in education didn’t start with homeschooling due to the virus. Education has been crying out for transformation for some time. MOOCs came along a while ago, starting with Stanford EPGY and Johns Hopkins, and quickly expanded to Coursera and other self-teaching platforms. More recently, companies like Lambda School, Monti Kids, and Kidz2Pros have transformed how education gets paid for, begins, and ties digital into the real world. Others have created new ways to technically train specialized professionals (Osmosis, TransfrVR). COVID simply accelerated this process and the winners here are those with the ability to respond to the demand with the best tech and courses. Perhaps the most dramatic recent innovation in education is ISAs (Lamda School), allowing students to pay for their education only as they earn higher income from the skills they learned in school. And in the K-12 space, additive learning platforms are accelerating digital adoption for home learning. All this being said, there will likely be a swing back to tradition here as parents learn to appreciate physical school even more, now that they’ve been forced into homeschooling. The strongest new education companies will become a part of the brick and mortar institutions as well as a part of the home. Our portfolio company Epic! epitomizes this duality.

Sustainability

Sustainability is a tricky category. The long term gain is obvious, but often unrealized in the first few years, making market dips tough on these businesses. Sustainability is often seen as earth positive (Novonutrients, Better Earth, Curie Co.), but we also look at the physical and emotional needs of humans as those relate to sustainability, like clean air (Ava, Wynd) and earth positive food production (Finless, Emergy). The fundamentals are more important here than ever (strong runways, clear problem to solve with significant long-term implications, fundamental to human existence). Without these three factors in place, this category as a whole may face challenges as it works to bring radical new products to market.

Last Thoughts

Our fund strategy rests on three fundamentals:

-

Find the best segments.

-

Find the companies in those segments differentiated by deep science, strong IP, or distinct product advantages.

-

Identify CEOs who blend vision with pragmatism and who are prepared to lead their teams through the unanticipated shifts and trials that lie ahead.

In health and happiness companies, as we define them, we have discovered one of the greatest investment areas in decades. The stability and growth showed by our companies during this, the worst of worst times proves that we have found the right science and leaders to win in good times and bad.

This post was written by Jun Deng and Holly Jacobus, Investment Partners at Social Starts and Joyance Partners and is republished with permission.