Steady seed investments prove a cautious but healthy market for healthy startups

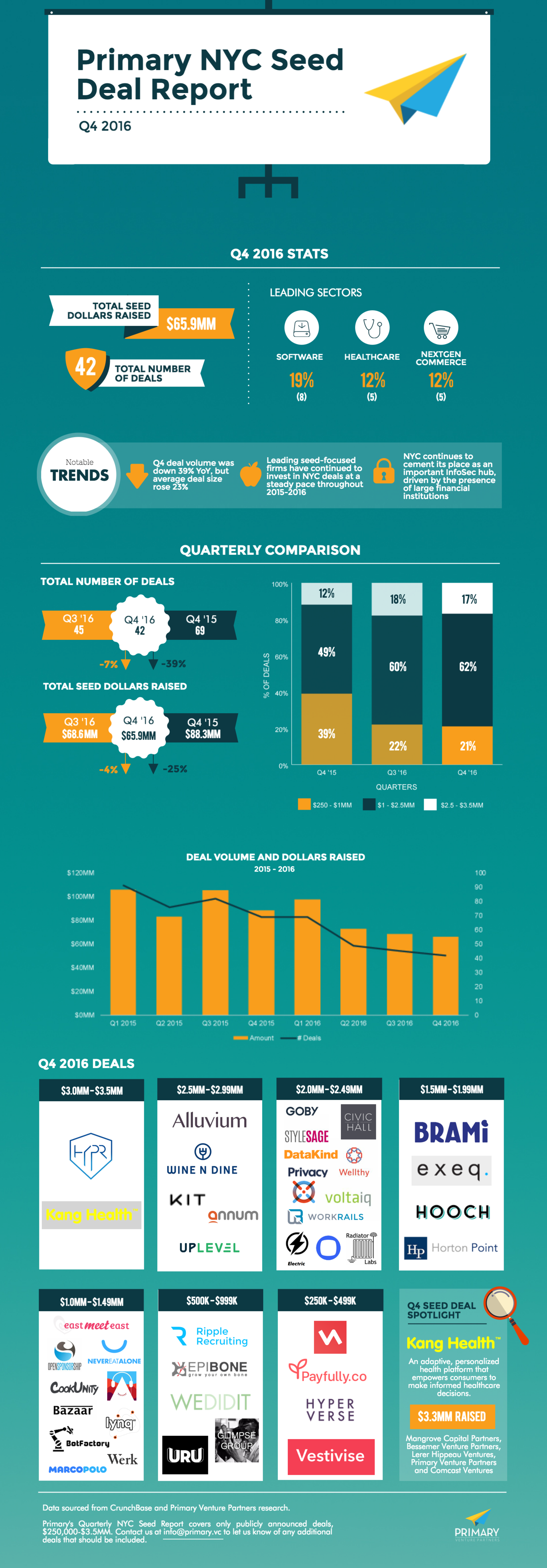

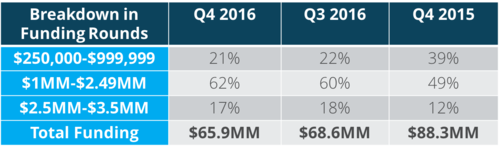

And so we have closed out 2016 not with a bang, but with a steady, if slightly muted, drumbeat that will herald the New Year with the promise of continued forward momentum. The quarter saw 42 seed deals in NYC, holding at a relatively steady pace from Q3 2016 but down 39% from Q4 2015. Total investment dollars were down just 4% from last quarter and 25% from this time last year.

WELCOMING THE NEW NORMAL WITH OPEN ARMS

While year-over-year comparisons might leave us feeling uninspired at the depressed state of 2016’s seed investment activity, it’s time to leave the past behind and accept that 2015’s furious check-writing and overly generous valuations were both unrealistic and unsustainable. Instead, we think the numbers we’re seeing now represent the market’s natural and healthy normalization around a still-robust, but considerably more rational equilibrium. So while deal volume is down significantly from this time last year, average deal size has increased by almost 25% since then, indicating that investors are eager to place larger bets on the most promising opportunities. In response, startups themselves have adopted a more conservative approach, focusing more on belt-tightening, sustainable operations and extending runways before subsequent financings, rather than aiming for rapid growth at all costs.

SEED FIRMS SHOW NO SLOWDOWN IN INVESTMENT PACE

In fact, in comparing the prior two years of seed investments across five leading seed-focused firms – First Round Capital, Lerer Hippeau Ventures, Primary Venture Partners, Greycroft Partners and Founder Collective – we see a relatively steady pace of NYC seed investments year to year. Collectively, the firms made 49 seed investments in 2015, a number that dropped just 16% in 2016, and is certainly not reflective of the more precipitous drop in overall deal volume witnessed in the NYC seed market as a whole. This suggests that while total deal volume may have declined substantially, there has been no corresponding drop-off in the volume of top-quality deals that the most prominent and active seed investors in the city are looking for.

INDUSTRIES TO WATCH

NEW WAYS TO PAY

Consumer financial services sees continued momentum, with funding this quarter going to new platforms that continue to challenge incumbents’ outdated user interfaces. Q4 saw funding for online payment platform Privacy, and Exeq, which helps users budget, save and invest with tailored recommendations.

The rise of the sharing economy has also brought about a new wave of financial products, such as Payfully, which offers a working capital solution for Airbnb hosts looking to collect payment quicker. Look for the continued maturation of sharing economy platforms to catalyze more of these products, though it’s unclear whether platforms like Airbnb will remain partners or competitors to these platforms over the long term.

SEEKING SECURITY AFTER A TUMULTUOUS YEAR

Will all the talk of Russian hacking and the U.S. election lead to continued interest in security deals by seed investors? In 2016, NYC became an important hub of infosec activity, driven largely by the presence of so many large financial institutions with complex security needs. In Q4, Privacy and HYPR both secured funding to help secure online transactions. And for when that hack does happen, Uplevel Security secured a round to help customers monitor intrusions and accelerate response times.

STREAMLINING CARE AND COMMUNICATION

The year has seen no shortage of healthcare startups aiming to improve coordination of healthcare services. Q4 saw continued proliferation of this trend, with funding for a number of tech startups aiming to improve access to services and communication tools that will create a better experience for specific patient populations. Annum Health targets those with alcohol abuse issues, while Wellthy’s mission is to coordinate care for elderly patients.

EAT YOUR HEART OUT, 2016

Food and beverage remains a category with continued early-stage investor interest, ranging from reinvented CPG brands such as Brami to software and content platforms that solve discovery (Hooch and Wine ‘n Dine) to sharing economy platforms like CookUnity. While seed funding for these businesses is abundant, there continues to be downward pressure for later-stage financings as many of these businesses struggle to solve issues of distribution and/or unit economics. It will be interesting to see how this new batch of food startups fares as they attempt to grow beyond the seed stage.

LOOKING AHEAD TO 2017

While the impacts of the 2016 election are yet to be seen, and may remain elusive for another several quarters, signs are pointing to continued steady forward momentum in NYC seed funding. While we don’t expect an immediate return to the pace of 2015 – investors’ bars have been appropriately raised, and we expect them to stay there – conversations with our seed investor peers suggest unanimity around continued enthusiasm for the seed opportunities NYC is serving up.