In the past few years, we have seen an explosion of venture capital investment into Financial Services (if you want to see data around dollar inflow into the sector, check out this report from CB Insights).

Although there has always been investment into Financial Services at some level, the types of companies receiving funding has changed. Payment technology has always received a relatively healthy dose of VC investment and has many notable successes to point to as a result (e.g. Dwolla, Square). Now, though, we are starting to see investment into a much broader range of financial industries, including wealth management, capital markets, and insurance.

VCs have often been accused of demonstrating a herd mentality when it comes to investing in new sectors. Based on a thesis, one firm decides to invest in a sector. When one of their investments begins to gain traction, the sector slowly becomes “hot,” with associates hunting for opportunities to put dollars to work. Although this herd mentality may be true, the Financial Services landscape is changing in a way that is making the industry much more VC-friendly.

For a long time, Financial Services was a human services industry: well paid individuals performing bespoke tasks and leveraging tightly held relationships to drive sales. But these sorts of people-driven businesses are notoriously difficult investments. They don’t scale, their value and clients leave with employees, and most of the revenue goes out the door, just to retain employees. There’s a reason why most law firms, consulting firms, and investment banks have been self-funded partnerships.

It’s obvious why the payments space has always received its due attention from VC – it’s an industry based on technology, not people. Technology scales. Technology can’t leave the company (unless you sell it), and technology doesn’t negotiate for a higher bonus.

Finance is undergoing an unprecedented shift, as technology stacks replace complex services traditionally performed by humans, and relationship-based business models are giving way to lower-cost electronic and web-based platforms. Payments is no longer the only sector within Financial Services catching the eye of venture capital—and we’re already seeing notable successes pop up outside of the payments world:

Lending Club is automating the previously highly manual underwriting process for personal loans, Betterment and Motif are creating self service models to allow consumers to construct their own portfolio strategy vs. relying on a financial advisor, and Estimize (a VSL company) is supplementing manual sell side research analysis with crowdsourced data (which is proving more accurate).

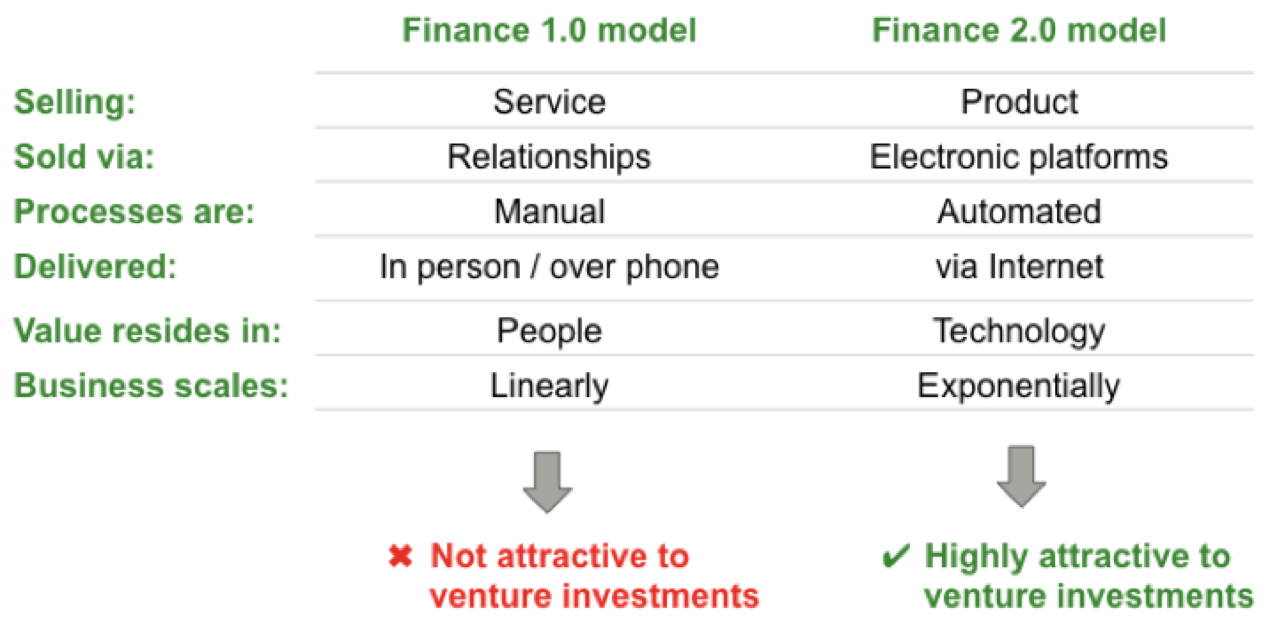

Below is a table that sums up the Finance 1.0 vs. Finance 2.0 business models and demonstrates how these new platforms are highly attractive to venture investment. Needless to say, these new business models are what we look for at ValueStream.